New Strategy, New Opportunities? What makes PayPal stock interesting for investors?

PayPal shares have come under heavy pressure in the recent weeks. However, the new strategy gives hope for more growth in the future.

I have been invested in PayPal stock for almost exactly 12 months. At that time, I published an investment story here on the substack entitled "PayPal Stock : The Sleeping Giant Awakes".

The timing of the entry in the spring of 2024 was good: PayPal shares rose more than 50% from March 2024 to the day of Trump's inauguration on January 20th, 2025. Since then, however, PayPal shares have fallen significantly. In the first six weeks of the Trump administration, the stock lost 25%, along with many other US tech stocks.

As a result, the PayPal position in my Long/Short portfolio lost all the book profit. Easy come, easy go?

It would be too easy to blame the erratic US politics alone for PayPal's share price weakness. After all, in addition to Trump's decrees, there have also been some new company figures to digest in recent weeks.

This PayPal stock analysis will therefore focus on PayPal's financial results for 2024, the initial guidance for 2025 and the new long-term goals that the company announced at an investor day in late February.

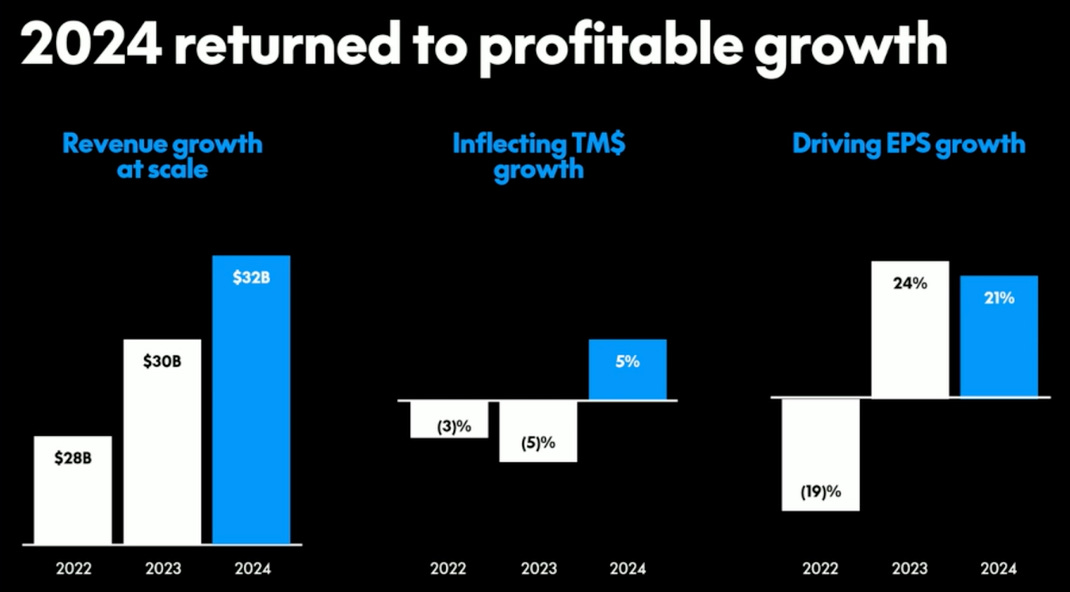

PayPal's 2024 Financial Results

The key financial results of PayPal for the year 2024 as compared to the previous year are as follows:

Revenue: PayPal's net revenue grew 7% to $31.8 billion in 2024, while Q4 revenue grew only 4%. This sounds disappointing, but it has to be viewed in the context of the (new) management's conscious and early announced decision to forgo unprofitable revenues immediately and therefore not to renew some contracts with merchants in the B2B business.

Operating Income: GAAP operating income increased 6% to $5.3 billion, representing a return on sales of 16.7%. Excluding restructuring charges, operating income grew at a double-digit rate of 14% to $5.8 billion, representing an operating margin of 18.4%.

Earnings per share: GAAP earnings per share rose only 4% to $3.99, disappointing the expectations of analysts. Non-GAAP earnings per share grew much faster at 21% to $4.65.

Free cash flow: The free cash flow, which is much more important to growth investors like myself, increased by 60% to $6.8 billion for the full year. Adjusted free cash flow was $6.6 billion, representing an increase of 46%.

These results show solid growth in several key areas, particularly free cash flow. After two tough years, PayPal returned to a profitable growth trajectory in 2024. The company also improved profitability with higher non-GAAP operating income and non-GAAP earnings per share.

However, the share price fell significantly following the release of these numbers.

Business Development Key Figures

PayPal's total payment volume (TPV) grew 10% to $1.68 trillion in 2024. In Q4, TPV growth was 7%.

Payment transactions: Payment transactions grew 5% to 26.3 billion for the full year. In Q4, this number decreased by 3%. The reason: PayPal had announced that it would focus on profitable transactions in its Braintree business with merchants, even if that meant less volume on the platform at the moment.

Active accounts: The number of active PayPal accounts increased by 2.1% to 434 million in 2024. Of particular importance is the increasing engagement of active customers. Specifically, the number of transactions per active account increased by 4%.

Strong Balance Sheet Enables Share Buyback

PayPal has a very strong balance sheet at the end of 2024. Cash reserves of $15.4 billion were offset by debt of $11.1 billion. PayPal returned $6.0 billion to its shareholders by repurchasing approximately 92 million shares. This reduced the number of shares outstanding by more than 7% during the year.

A new $15 billion share buyback program was announced in February 2025. At the current share price of under $70, this could repurchase approximately 20% of all outstanding shares.

The number of shares outstanding is therefore likely to continue to decline significantly in the coming years, despite industry-standard share-based compensation ($1.2 billion in 2024).

PayPal Guidance 2025

PayPal has not issued a revenue target for fiscal year 2025, but has stated a minimum growth rate of at least 5% for transaction margin dollars.

Analysts expect revenue growth of 4%, as in Q4 2024.

Non-GAAP earnings per share are expected to grow 6-10% in 2025. GAAP EPS is expected to be $4.80 to $4.95, representing EPS growth of just over 20%. As in 2024, the large share repurchases are expected to contribute to this significant increase.

Free cash flow is expected to be in line with 2024 at $6-7 billion, with nearly all cash flow (approximately $6 billion) to be returned to shareholders through share repurchases.

PayPal's longer-term strategy was presented at an investor day on February 25th, 2024. Here are the key announcements and insights:

The Launch Of PayPal Open

The PayPal platform has been a hodgepodge of products and technologies for many years. The numerous products it has acquired have never been properly integrated. It is not a single technology platform in the true sense of the word. On the consumer side, PayPal and Venmo are joined by the money transfer service Xoom. On the merchant side, there are Braintree, PPCP (PayPal Complete Payments), Zettle, and many more, all with different backend systems.

A single user who uses multiple PayPal products is registered with PayPal under different user profiles. This prevents synergies and slows down innovation in the business. Standardizing user profiles is the only way to fully personalize the user experience across products.

The new management is now finally tackling the long overdue consolidation and developing a single open backend called "PayPal Open" by 2026. In the future, all systems will run on this new platform.

In the future, customers and partners should be able to program all products based on a single API. This should be a standard practice for a digital platform company. But at PayPal, this kind of open technology was neglected for many years. In my opinion, this is the main reason why younger and organically grown competitors (such as Stripe) have been able to take market share from PayPal in the B2B business.

But better late than never. PayPal's management has recognized the weaknesses and is currently developing the "PayPal Commerce API" as part of "PayPal Open". This will provide access to 80 million consumer profiles in the US right from the start.

The Dual-Brand Strategy With PayPal And Venmo

All products, with one exception, will be sold under the PayPal brand. Acquired brands like Braintree, Zettle and others will eventually become a fading memory.

One exception is Venmo. This P2P payment service, which is free in its basic function, is incredibly popular among younger people in the U.S. and has 62 million monthly active users.

The Venmo brand is cool and is increasingly used in the US as a verb for sending money. It is therefore very understandable that PayPal's management has opted for a two-brand strategy. Venmo is to be expanded in a targeted manner, and the large Venmo user base is to be monetized much better than before through payment services and a debit card.

Specifically, Venmo is expected to generate more than $2 billion in revenue by 2027. That would still be a modest 5-10% share of revenue. For me, this raises the question of whether a second brand is really worth the effort.

PayPal Outlook To 2027

At the Investor Day, PayPal's management communicated the following mid-term goals for the period up to 2027:

Payment volume processed through PayPal is expected to grow faster than the overall e-commerce industry through 2027.

Payment volume is expected to grow by approximately 7-9% p.a. through 2027, with the company deliberately avoiding low-margin sales. In the long term, the company aims to return to double-digit growth.

Operating expenses are expected to grow at less than half the rate of payment volume.

Earnings per share (non-GAAP) are expected to grow by more than 10% per year until 2027, and by more than 20% per year thereafter.

Cash flow should grow in line with net income, with 70-80% of free cash flow preferably returned to shareholders through share buybacks.

I think these goals are ambitious, but with the new management and the focus on improving the underlying technology platform, I believe they are realistic.

Valuation Of PayPal Shares

Many analysts are skeptical about PayPal's ability to achieve these ambitious goals. Many believe that the ever-increasing competition from Apple Pay and Google Pay, among others, is too strong. As a result of the mixed analyst opinions, PayPal stock is once again very cheap in March 2025, at least if you use the cash flow multiple as your primary valuation metric, as I do.

At just under $70, the ratio of free cash flow to enterprise value is 10. I think this is very appealing; PayPal stock has only been this cheap once in recent years. That was in August of 2024, which was followed by a 50% rally in two quarters. Will history repeat itself?

An investment in PayPal shares at this time is first and foremost an investment in the new management team around Alex Chriss. I believe he has set the right course in his first year as PayPal's CEO. I am very optimistic that he will be able to restructure and modernize the aging PayPal platform in a way that will enable innovation and growth in the future.

In the medium to long term, I believe PayPal stock will return to well over $100. But shareholders need to be patient. It simply takes time to get a giant like PayPal, which has been mismanaged for years, back on a profitable growth path.

If you want to keep an eye on PayPal with me in the future, you can subscribe to my free newsletter here:

*Disclaimer: The author and/or related persons or entities own shares of PayPal. This PayPal stock analysis is an expression of opinion and not investment advice.

Thanks for the great article,

paypal honey is a possible red flag even though revenue contribution is miniscule as per some estimates ?