IAC Holding: Is the Next Billion-Dollar Spinoff on the Horizon?

Investing in IAC today is like getting a dollar for 50 cents. This is what makes IAC a high-conviction stock in my portfolio.

While most retail investors think of big tech stocks from the Magnificent Seven or currently hyped AI stocks among tech small caps, an old acquaintance slumbers in the background of my portfolio, largely unnoticed: the IAC Holding IAC 0.00%↑ .

Longtime readers of this substack are familiar with media mogul Barry Diller's holding company, IAC, not least because of its previous spinoffs. Match Group, Vimeo, and Angi all originated from the IAC stable. The strategy is to buy or build companies, then make them big and spin them off.

Following the spin-off of the home services platform Angi in March 2025, IAC Holding is once again particularly streamlined. Its portfolio contains only a few large holdings, making it easier to analyze IAC shares. This is interesting because IAC's market value has significantly lagged behind its actual net asset value for some time.

Why Traditional Key Figures don't work – and SOTP is the Better Lens

Anyone looking for a fair price-to-earnings ratio or EBIT multiple at IAC will be disappointed. The holding company's structure is too complex and convoluted. The only way to determine the actual value is through a sum-of-the-parts analysis (SOTP). This involves valuing each investment separately and adding up the totals. This reveals how much IAC is actually worth as a whole and whether the current share price reflects that value.

My current analysis yielded astonishing results: IAC's intrinsic value is over US$6 billion, yet the stock market values the company at just over US$3 billion. This corresponds to a discount of approximately 50 percent. Such a large discrepancy is unlikely to persist in the long term.

What's in there? IAC's investments:

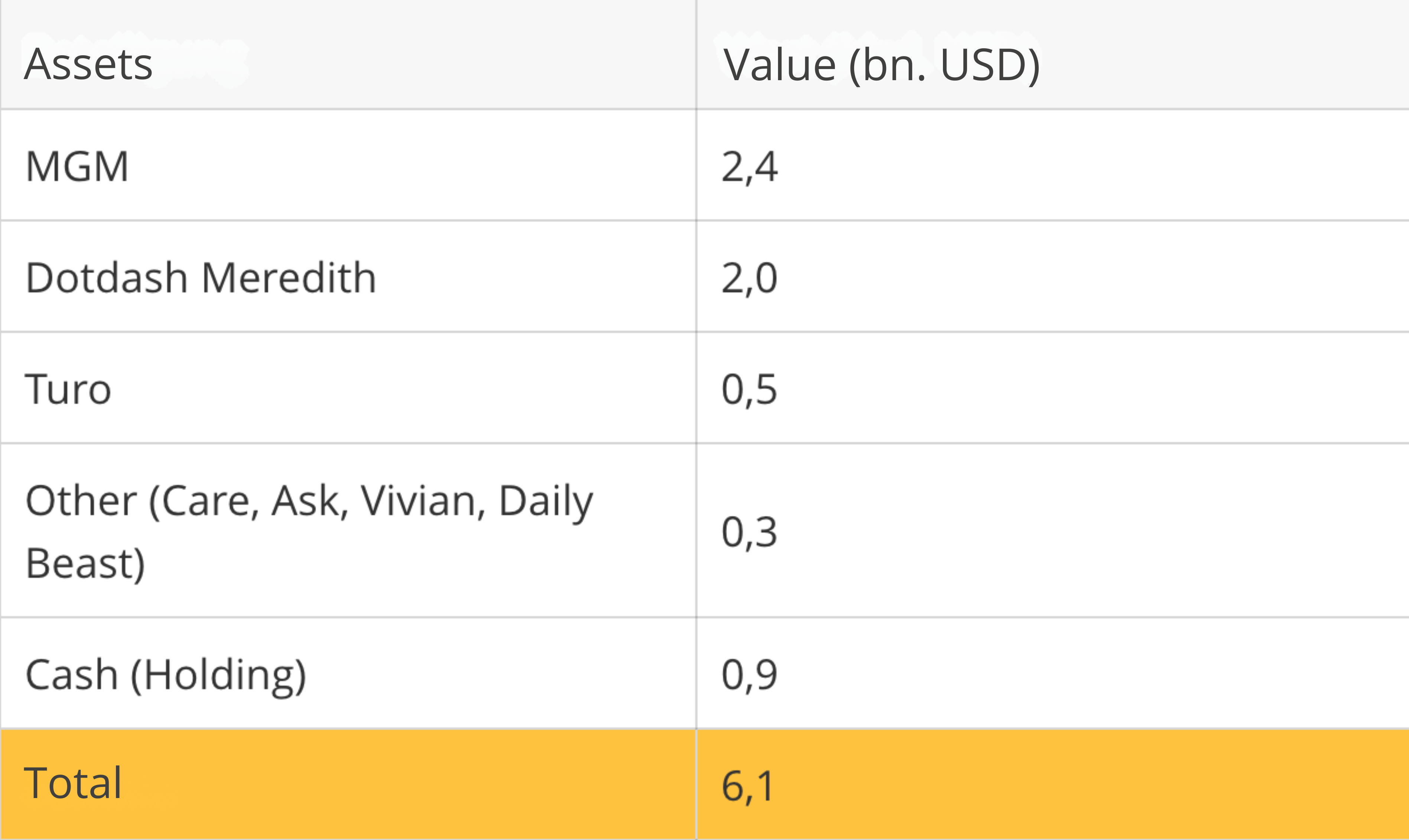

Following the ANGI spinoff, IAC's core business consists of three major investments: a significant stake in casino giant MGM Resorts, publishing subsidiary Dotdash Meredith, and an investment in car-sharing startup Turo. These investments are complemented by smaller platforms, such as Care.com, as well as a substantial cash reserve at the holding company level.

MGM – a Reliable Anchor in the Portfolio

IAC is MGM Resorts' MGM 0.00%↑ largest shareholder, currently holding around 64.7 million shares, corresponding to approximately 23 percent. At the current price of just over US$37, this stake is worth around US$2.4 billion. This value can be verified on any trading day, as MGM is listed on the NYSE.

More interestingly: MGM has run an aggressive share buyback program for years, repurchasing nearly half of its shares in the last five years. The more MGM buys back from the market, the larger IAC's relative share becomes — without IAC taking any action.

Although MGM is no longer a genuine growth company, a significant jump in earnings is still expected in a few years. Construction of MGM Osaka, a massive hotel and casino complex, began in Japan in April 2025. Once it opens in fall 2030, the complex could become MGM's dominant profit center.

Although there are a few years before the opening, at some point in the coming years, the market will likely react to the significant earnings potential of the new Japanese operations. MGM has signaled EBITDA expectations of over USD 2 billion annually, which would represent an 80% increase from 2024 levels.

MGM also has a promising player in the booming US online casino market with BetMGM. After several years of losses during its development phase, the 50:50 joint venture with Entain will generate positive EBITDA of at least $100 million for the first time in 2025, with revenues exceeding $2.6 billion.

Given these future prospects, MGM shares are certainly not overvalued, with a current cash flow multiple of 13.

Dotdash Meredith – an Underrated Digital Publisher

A second key pillar in the IAC portfolio is Dotdash Meredith. In 2021, IAC acquired the long-established U.S. publisher Meredith and combined it with its own Dotdash digital brands. The goal was to create a powerful digital content group.

Indeed, the company has stabilized after several difficult years and is targeting adjusted EBITDA of around $350 million on revenue of $2 billion in 2025. I value Dotdash Meredith at nine times EBITDA, corresponding to an Enterprise value of $3.2 billion. After deducting approximately $1.2 billion in net debt, the equity value is around $2 billion. For reference, IAC paid $2.7 billion for Meredith in 2021.

Although Dotdash relies heavily on digital advertising revenue and must pay 7.6% interest on its restructured debt, its proprietary D/Cipher targeting platform gives it a significant competitive advantage, even in the "cookie-less" AI era. In my opinion, its operating potential is far from exhausted.

Turo – the Hope for the Future

Less prominent but equally exciting is IAC's approximately 32 percent stake in Turo, the leading peer-to-peer car-sharing platform often referred to as the “Airbnb for cars.” Turo had planned to go public in 2022 but has postponed its IPO several times due to the challenging market conditions.

Currently, Turo is valued at "only" around $1.45 billion in the pre-market, following a significant price decline in connection with the failed IPO plans, which leaves IAC's stake at around $500 million.

If the stock market window reopens and Turo successfully goes public, this investment could regain significant value. Another potential outcome is a takeover of Turo by a company like Uber. I outlined my thoughts on this in the Uber Investment Story.

Other Smaller Assets

In addition to the three large blocks, IAC owns digital platforms such as Care.com, Ask Media Group, and Vivian Health. These are not listed on the stock exchange, and they are not huge when viewed individually. However, together they generate solid revenues of over US$500 million and positive cash flows. Due to the significant loss in value of such online assets, I am assigning a cautious value of around $300 million to this package, which is more conservative than optimistic.

Cash

An often-overlooked value driver is the cash holdings at the holding company level. IAC currently has more than $900 million in cash that is not tied up in subsidiaries. Management can use this capital for share buybacks, new investments, or debt repayment. This financial flexibility is a significant advantage, especially in an uncertain market environment.

IAC's holdings at a glance:

The net asset value of over USD 6 billion currently contrasts with IAC's market capitalization of only USD 3.2 billion. This is based on an IAC share price of just over USD 40 and 80.1 million outstanding shares.

The MGM stake and cash reserves held by the holding company alone exceed IAC's current market value!

Why is IAC trading at such a significant discount?

Despite IAC's clearly identifiable value, the market has yet to recognize it, even after the Angi spin-off. There are several reasons for this.

First, IAC suffers from the classic conglomerate discount. Investors today prefer focused business models — companies with multiple holdings are considered confusing and difficult to value.

Second, there are concerns about corporate governance. Barry Diller, now 83, retains control through preferred shares with multiple voting rights, making institutional investors skeptical.

Third, the portfolio has not been entirely successful recently. Some investments, such as Care.com and Dotdash Meredith, are trading well below IAC's entry price. The spin-offs, Match Group (2020) and Vimeo (2021), have underperformed since their respective splits. No clear trend has yet emerged for the latest spinoff, Angi (2025).

Fourth, the economic environment also plays a role: digital advertising is cyclical. When companies cut advertising budgets, platforms such as Dotdash Meredith are impacted immediately. Additionally, many classic online platforms in the IAC portfolio are considered losers in the upcoming AI era.

What needs to happen for the value to increase?

Despite these challenges, a number of catalysts have the potential to significantly increase IAC's share price in the medium term.

First, an IPO or spin-off of Dotdash Meredith would be a significant factor. If the company were listed separately on the stock exchange, its value could be presented much more transparently. Such an event could easily unlock $1-$2 billion in additional market value, triggering a jump in the IAC share price.

Turo remains a potential catalyst as well. As soon as the IPO window reopens, the platform could quickly go public. Its value could rise significantly with the tailwind provided by new mobility trends or a takeover (e.g., by Uber).

Share buybacks should not be underestimated, either. IAC has an ongoing authorization to buy back 10 million shares, which corresponds to nearly 15 percent of the free float. If these buybacks are implemented consistently, they should positively impact the share price.

Risks that investors should keep an eye on

Despite all the opportunities, IAC is not a risk-free bet. The digital advertising business remains cyclical, and potential disruption from AI is difficult to predict. Some investments are illiquid, and Dotdash Meredith's interest burden of around 7.6% is high.

Let's be honest: Barry Diller has not always had perfect instincts in recent years. He is now 83 years old, and it certainly did not help IAC's share price in 2025 that he took on more operational responsibility as Executive Chairman following Joey Levin's departure as IAC CEO.

Conclusion: A Clear Case for Value Investors

IAC shares are not a speculative investment for the next quarter. However, at today's price, they are an exciting long-term investment for patient investors looking for value in the tech sector.

IAC Holding's intrinsic value is clearly above the current stock market price, and the balance sheet offers downside protection. Strategic decisions that could be made at any time, such as a spin-off or IPO of Dotdash Meredith, could create significant value.

In short, anyone who buys IAC today is essentially buying a dollar for around 50 cents, securing both substance and strategic options for the future. In a market where growth stories are often overvalued, this is a rare opportunity. IAC therefore remains a core investment in my portfolio.

If you would like to follow IAC in the future together with me, please subscribe to my free Substack here:

*Disclaimer: The author and/or related persons or companies own shares in IAC and Angi. This article is an expression of opinion and does not constitute investment advice.

IAC could do a Split-off: offering some of their shares in MGM for their own shares. The exchange rate should be favorable so that IAC shareholders are inclined to tender. Any thoughts?