Alphabet Stock in AI Frenzy: Still a Buy at All-Time-High?

Alphabet Stock in AI Frenzy: Still a Buy at All-Time-High?

An update on the Google parent company's shares following the convincing figures for Q1 2024.

What have we not read in the past 18 months since the launch of ChatGPT about the questionable future of Alphabet in the age of AI: The dominance of the Google search engine would be threatened by the growing market share of Microsoft Bing. Google's own LLMs for training GenAI applications would be left behind in the competition with OpenAI. Waymo could lose its leadership in autonomous driving, etc.

Alphabet has now not only reported very good Q1 2024 results, but also managed to allay these concerns, at least for the moment, with a convincing earnings call. Alphabet's share price rose by double digits on the news and is at a new all-time high as I write.

Here is my take on Alphabet, which has been the only big tech stock in my sample portfolio for some time.

The Alphabet figures for Q1 2024

Google increased its revenue by 15% compared to the same quarter last year. There was double-digit growth in almost all businesses. YouTube Ads were particularly strong at +20% and Google Cloud Platform, which saw revenue growth of 28% to 9.6 billion USD. There was also an impressive 72% increase in revenue from 'Other Bets' to 500 million USD. This includes the Waymo autonomous driving business.

Despite its efforts to diversify its revenue streams, Google's search engine still accounts for 57% of Alphabet's total revenue. This share is declining very slowly as Google's search business continues to grow at double-digit rates. A real luxury problem?

Even more important for the share price than the revenue trend is the fact that Alphabet has its escalating costs from 2022 under control again. Of course, the large number of layoffs from 2023 have contributed to this. I am optimistic management learned from the over hiring mistakes they made back then.

Alphabet's operating margin in Q1 2024 was a whopping 32%, up from 25% in the prior-year quarter. That equates to an operating profit of over 25 billion USD.

Free cash flow was significant lower at just under 17 billion USD. This was due to high cap-ex (12 billion USD), these are investments mainly in additional data centre capacity. Like Meta and Microsoft, Google is investing heavily in additional AI infrastructure. This is in response to the boom in new GenAI applications, which will be run by numerous software vendors on the Google Cloud Platform.

Alphabet's net margin was over 29% and earnings per share jumped over 60% to 1.89 USD in Q1 2024.

Google Cloud Platform (GCP), which has achieved a remarkable turnaround in profits over the past two years, also contributed to the excellent results. Operating income from Google Cloud multiplied to 900 million USD year on year, representing a margin of almost 10%.

The persistence and years of investment in GCP are now paying off. Google Cloud Platform's ease of integration and openness has given it a strong position in the start-up scene, even against the market leaders Microsoft Azure and AWS.

The position of Alphabet stock in the AI hype

In previous posts, I have argued that investor euphoria and expectations regarding the monetization of AI have become too high. I would even speak of an AI bubble that will burst sooner or later. See also: Is Nvidia a good investment for the next 10 years?

After chipmakers (i.e. Nvidia), the cloud providers such as Microsoft, Amazon and Google are now experiencing an AI-driven boom in their cloud services. Their customers are the countless application software vendors who are currently launching a plethora of new GenAI-driven SaaS products. Behind this trend are the various 'AI copilots' that are now finding their way into many software applications.

The unanswered question now is how much money can really be made ADDITIONALLY on the application software side with these new GenAI products. How much value do these AI assistants really add? What are consumers and especially businesses willing to pay for these services? And won't the increased efficiency of AI ultimately lead to an increase in software revenue per user, but with fewer employees being licensed?

I expect there will be a lot of disappointment from application software vendors in the next 1-2 years. This will ultimately have a negative impact on the business of Nvidia and the cloud providers. The AI hype will end sooner or later, just like any other hype.

Google will also be negatively affected. But to a much lesser extent than, say, Nvidia, whose business development is much more directly based on these AI sales.

Share Buybacks and Dividends

I speculated about it here in early February, but just one quarter later it is a reality: following Meta Platforms, Alphabet will now start paying a dividend. The first quarterly dividend of 20 cents will be paid on 17 June 2024, which represents a rather symbolic annualized dividend yield of 0.5%. This makes Alphabet shares investable for the first time for all the investors, who generally only invest in dividend payers.

There is also a new 70 billion USD share buyback program, which would allow Alphabet to buy back 4% of its outstanding shares at the current price.

In recent years, Google's parent company - like Apple and Meta - has bought back a lot of its own shares. The number of Alphabet shares outstanding has fallen by 7% over the past three years.

The valuation of Alphabet shares versus Microsoft

If you have been following this Substack for a while, you will know that a reasonable valuation is fundamentally very important to me whenever making an investment.

Valuation matters!

I think you can compare Alphabet to Microsoft quite well. Both companies have weathered a period of slow growth and are now capitalizing on the AI boom, growing again at double-digit rates. That in itself is outstanding given the sheer size of the two tech giants.

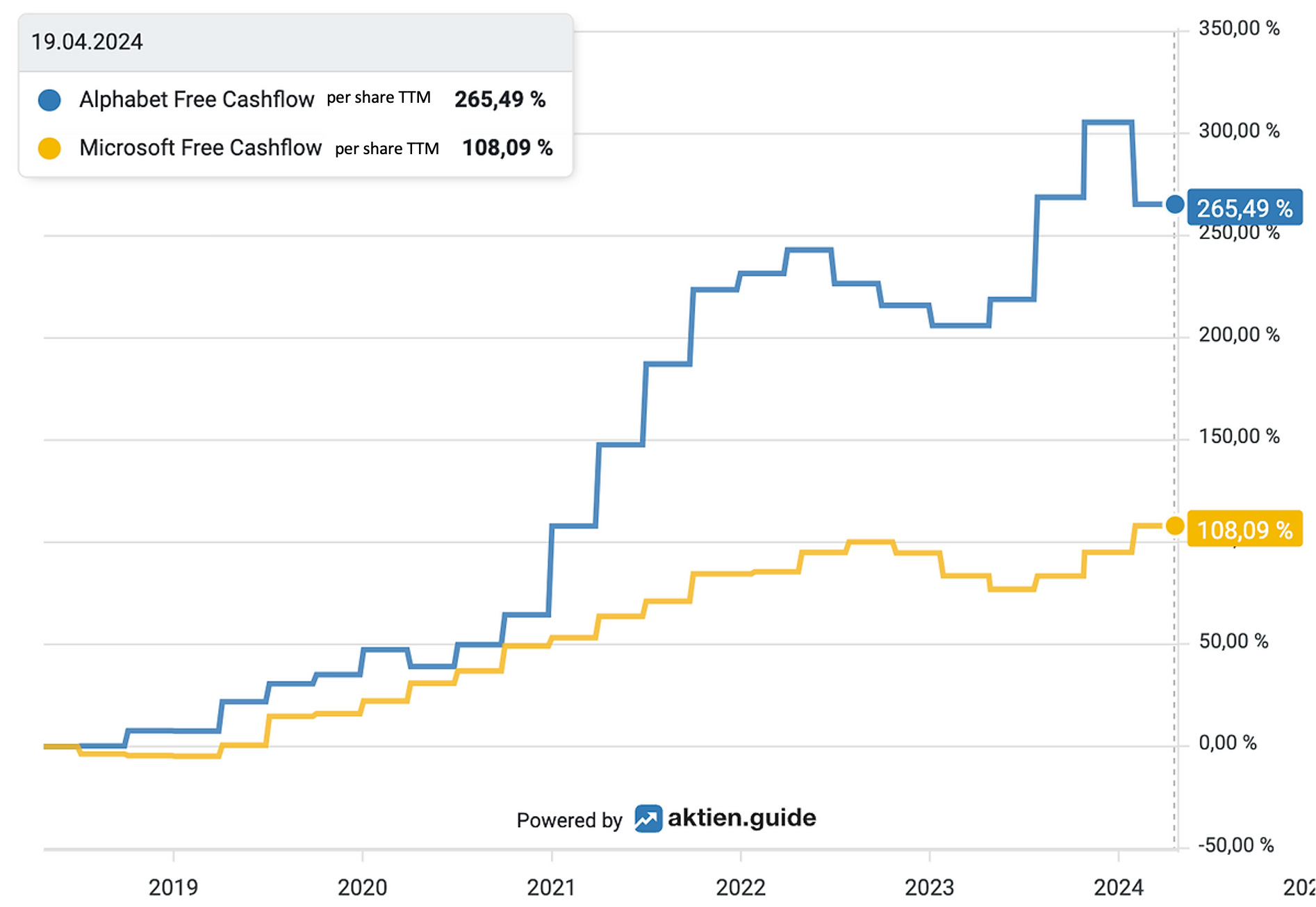

Microsoft's margins have always been significantly higher than Alphabet's. In this context, it is interesting to note that Alphabet's cash flow performance has nevertheless been significantly stronger than Microsoft's in recent years.

Alphabet's free cash flow per share has increased by more than 250% over the past 6 years, while Microsoft's has 'only' increased by a good 100%.

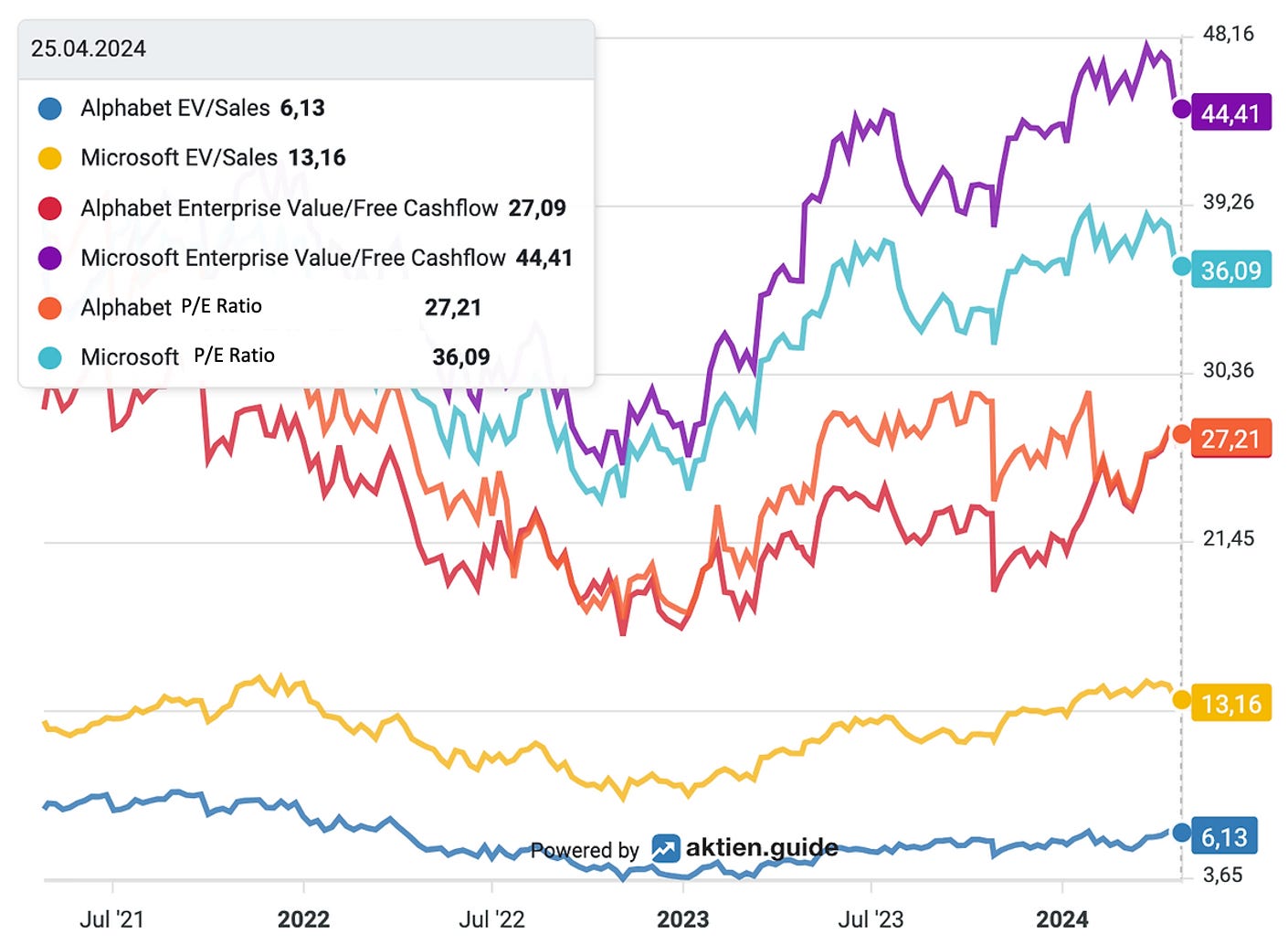

Nevertheless, Microsoft is significantly more expensive than Alphabet: Each dollar of Microsoft revenue is valued more than twice as highly (EV/Sales 13) as a dollar of revenue at Google's parent company (EV/Sales 6).

This reflects the fact that Microsoft has a high proportion of recurring revenue, which is particularly highly valued by the stock market. In contrast, the financial market seems to believe that Google's business model, with its focus on advertising, is much more fragile and that this revenue stream is therefore worth less.

Microsoft is also valued much higher in terms of the multiple of net income (P/E 36 versus 27) and free cash flow (EV/FCF 44 versus 27). In my view, such a large valuation discount for Google's business model is clearly excessive.

Conclusion

I think Microsoft stock is overvalued and clearly at risk for a pullback once the market's inflated AI expectations are corrected.

I do not see Alphabet shares as undervalued either. However, the stock is still reasonably fairly valued and remains a hold for me - as it has been for years.

I expect Google to continue to play a leading role in the age of AI and remain comfortable with my Alphabet investment. I am therefore not thinking of realizing the book profits of over 300% in my investable model portfolio. At least as long as Alphabet's valuation remains moderate and does not get caught up in the AI hype.

If you want to follow Alphabet, Microsoft and Co. with me in the future, you can

*Disclaimer:

The author and/or associated persons or companies own shares in Alphabet. This article is an expression of opinion and does not constitute any investment or financial advice.

Good insight. Was weird ppl looked at the extra capex as a bad thing - literally only doing it since they see huge demand for Google Cloud. Lot of question marks around search revs for me but for ad spend and not that the search engine won’t continue to be a monopoly.